What is The Minimum CIBIL Score for Business Loan? This key point is important for entrepreneurs that want to have funding. We will continue this trend, as we jump straight into the how CIBIL scores impact approval of business loans (Getting a little more specific), and how you can increase your CIBIL score and apply for that business loan.

Minimum Credit Score Requirements for Business Loans

Varying Requirements

How Good of Credit Do You Need for a Business Loan? Therefore, it is important for all the small business owners to understand the differences between these requirements as it may directly impede their borrowing potential. Any applicant who failed to fall within the specific credit score range that a particular lender set was at great risk of denial for a business loan.

Importance of Understanding Specific Requirements

For small firms in need of loans, familiarizing themselves with the precise credit score requirements of various lenders is vital. Small business owners can simply seek out the institutions for which they are likely able to qualify and apply only to those lenders– armed with a better understanding of what credits score is required for each one.

Ready to Scale Your Business? Find out how our custom-made business loan in Coimbatore can help, irrespective of your CIBIL score. The time to unlock the growth, is now.

Importance of CIBIL Score for Business Loan Eligibility

Key Role

- The minimum CIBIL score plays a very important role in the loan eligibility of the business.

- CIBIL score is the most important parameter for lenders to judge the creditworthiness of a business.

- A better CIBIL score reflects better the business financial responsibility and increases the chances to gain a loan.

- It is the most important for the businesses seeking favorable terms at higher loan amounts to keep their CIBIL scores.

- This makes it look like the borrower is a responsible person who can handle money and borrow money that they will pay back, even when they are not in a stable job.

Impact on Loan Terms

- A higher CIBIL score will assist businesses get loans at lesser interest rates for more extended repayment tenor and a more significant amount of principal.

- In addition, the CIBIL score may also use in conjunction with the conditions and maybe some other information on the loan approval process itself faster and reduce supporting documents needed.

- Applicants with excellent credit histories are automatically perceived to be more responsible potential borrower and more likely to be approved and will save hours of paperwork.

Impact of Credit Score on Loan Terms and Interest Rates

Influence on Loan Terms

- Realize that your credit score plays a large role in the kind of offer you get for a business loan as a borrower.

- This is because a higher credit score typically equates to a better loan, such as a lower interest rate or a higher borrowing amount.

- At the same time, businesses with weaker credit scores may find the lending terms to be less forgiving and with higher interest rates.

- A positive score widens the range of borrowing amounts and improves repayment conditions, while a lower score restricts loaning opportunities providing unfavorable repayment terms.

- Conversely, those with bad credit history may be limited to significantly smaller loans with very short terms and interest rates that are almost impossible to justify.

- This difference magnifies the importance of having a good credit score, in particular when you think about seeking business funding.

Impact on Interest Rates

As a borrower communicates his creditworthiness to a financial institution, that has an impact on the different interest rates that one may be able to get from a lender. When your borrowers have a positive track record, they can get loans at low interest rates, which means the less expensive borrowing costs for them throughout the life of their loan. Negatively, marks found on a credit file can push up the cost of borrowing due to lenders assessing an increased risk.

Pros:

Basically, higher credit scores mean better loan terms.

- Business loans at scale at better terms of repayment.

Lower interest rates are available to those with good credit – either individual or business credit histories.

Cons:

People with low credit scores may find it challenging to find borrowing opportunities.

Historical poor credit history results in probably limited availability and harsher repayment terms.

Higher borrowing costs for individuals and businesses with blemished credit

Strategies for Qualifying for a Business Loan with a Good Credit Score

Demonstrating Financial Stability

- A good credit can be maintained by simply paying off the existing debts on time and avoiding frequent usage of credit.

- This is because the CIBIL score is a measure of financial responsibility as far as the lenders are concerned.

- When businesses exhibit good financial habits on a regular basis, e.g. paying their bills on time and managing their debt responsibly, they can greatly improve their odds of getting approved for lower cost loans.

- When looking to secure a business loan, be sure that you have a business plan in place and are providing solid revenue projections.

- Banks are likely to give the green light to businesses that can demonstrate detailed plans on how to succeed in the long-term.

- A good credit score combined with the use of collateral or a personal guarantee can help your loan application significantly.

- This collateral secures the lender in the event that the borrower defaults on the loan

Leveraging Strong Relationships with Lenders

- Otherwise, good credit scores assist them in getting business loans on favorable terms by establishing strong relationships with lenders.

- By keeping channels with the banks or financial institution open, businesses see the plethora of lending options available on them in context to their creditworthiness.

- Building this trust by providing these existing partners with more transparency on the goals of the business and also financial information on how the business is running will allow these companies to be in a good place when turning to these relationships for financing opportunities.

Options for Securing a Business Loan with a Low Credit Score

Alternative Lenders

The requirements of the latter lenders were narrower, and they can take into account a wider range of tests concerning borrower quality controlling. The lending criteria of alternative lenders are also often easier to meet and decisions can arrive in a fraction of the time compared to banks.

Although the interest rates are usually not low, non-traditional lenders make funds available to the businesses that desperately need them but are locked out of traditional markets due to low credit scores.

Specialized Financing Programs

Another way to get a business loan with bad credit is to find specialized financing programs. There are programs some cater to businesses that have credit challenges where they have financial products and services specifically suited for you. These programs know that a lot of small businesses have credit issues and are still doing business every day.

Secured Loans

For applicants with poor credit, secured loans are attractive since they offers business fund at a very low cost. Unlike unsecured loans where the sole thing that creditors can come after is your creditworthiness, secured financial loans are backed by security, such as a home or equipment, to protect against a default. This makes investing in the lender saving the credit card firm a bit of danger, that is exactly the reason why an individual with credit ratings could possibly be authorized.

There are also opportunities of secured loan provided by individual investors who can fund the businesses though peer-to-peer (P2P) lending platform, based on their potential with an alternative method rather than a credit history. P2P lending have risen from other sources of financing as a result of this, is a good choice where the borrower connects directly with the investors online and does not have to go through the traditional financial institution process.

Community Banks and Credit Unions

If you have a poor credit score, establishing relationships with local banks or private lenders can create opportunities. The local financial institutions place greater emphasis on personalized service and are more willing to deviate from the strict underwriting adherence to standardized guidelines from larger banks.

Improving Your Credit Score for Higher Business Loan Approval Chances

Regular Monitoring

- Checking your Credit Report Checking your credit report regularly is important for determining your credit score.

- If you monitor your credit report, you can catch the negative articles that are pulling your score down. For example, missed payments, excessive credit card debt or inaccuracies on the report

- Once you know what the bad influences are on your score, start fixing them.

Key Strategies

- And the number one strategy for improving one’s credit score: Timely Payments Timely payment of all the present accounts goes a long way in improving the credit scores.

- Debt Reduction Reducing the amount of debt owed can significantly enhance your credit score over time.

- Debt Reduction Cutting back on excessive debt levels will improve your credit score in the long run.

- When you pay off existing debts and maintain low balances on revolving lines of credit such as credit cards, you are proving that you can manage your finances responsibly, which in turn, raises your overall credit-worthiness.

- Do Not Overdo On Credit Inquiries Want to maintain the higher credit score, never apply for many new lines of credit in a quick time period as every single inquiry results in a hard pull on the report.

Professional Guidance

- Seeking professional assistance through certified counselors or reliable financial management tools would allow insights into enhancing and managing one’s personal finances efficiently.

- Personalized guidance, specific to unique situations and designed to help improve overall financial wellbeing through actionable next steps.

- Tools for Tracking Financial Health A lot of online platforms and mobile apps are available which are created with the only intention to help the customers tracking their personal finance efficiently.

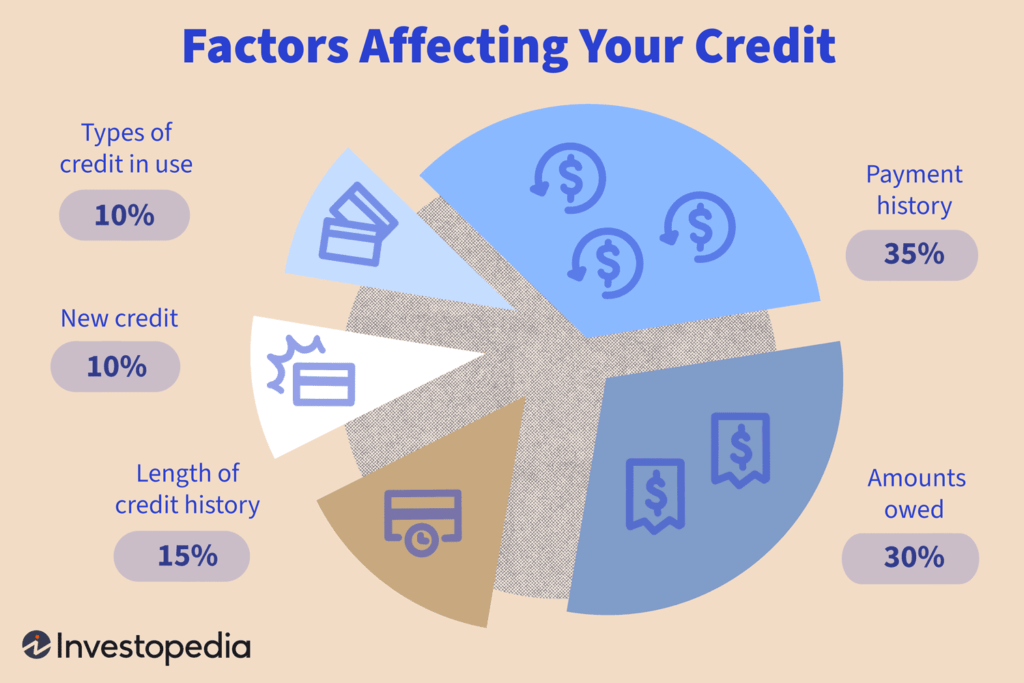

Factors That Affect Your Credit Score for Business Loans

Payment History

Building a track record of paying bills on time consistently shows that you are a financial reliable for potential lenders. For instance:

Meeting monthly utility expenses on time

Pay Credit Card Balances in Full Every Month

Credit Utilization and Length of Credit History

- Credit utilization ratio is the percent of available credit you are currently using.

- And here the less this rate, the better for us, that is we do not bring credit cards to the maximum.

- Demonstrate more financial responsibililty for a longer period of time and this could go a long way to improve your creditworthiness because you will be able to show that you can borrown responsibility over the long haul.

- Such factors could include keeping old accounts open even if they are rarely used, and alternating newly-opened accounts in a short span of time.

New Credit Inquiries and Types of Credits Used

Every time you apply for a new credit cards or loan, you get what is called a “hard inquiry” on your report. Several hard inquiries in a short period of time are a red flag for lenders, who could read it as a sign that you are experiencing financial hardship. In addition to this, using different types of credit (mortgage loans, car loans, etc) demonstrates the fact that you can handle different types of debt responsibly.

Exploring Alternative Financing Options Beyond Traditional Lenders

Venture Capital

It consists of investors giving money to a startup or small business in exchange for ownership. Not like banks which are strict and tends to be risk-aversed, venture capitalists search excessive-development doable and prepared to be danger stakeholders with revolutionary concepts. Nevertheless, getting that giant venture capital cheque has to be matched with a decent business plan, a massive market opportunity and room for outsized returns.

Venture Capital:

Invests for Equity

Needs a great business plan and a significant market opportunity.

Angel Investors

As an individual who invests his money to an early-stage business for ownership equity or convertible debt.

While they do allow more flexible terms than traditional lenders, they generally require some kind of influence on running the business. Angel investors, although they are usually willing to invest in innovative ideas where a bank or more traditional lending institution might not, in general development better return on investment.

Angel Investors:

Actively invest personal capital into seed stage businesses

Seek participation in decision making

Crowdfunding

Crowdfunding is a basic model that enables entrepreneurs to use their networks to generate funds by inviting numerous people to donate funds (usually features a relatively small group of people who are given investment opportunities). It is an alternative way for businesses to raise capital and offer their products or services directly to consumers contributors.

But effective marketing and an impactful pitch that appeals to the target audience is necessary for a successful crowdfunding campaign.

Crowdfunding:

Requires many partakers to the financing

Hits Depend On Proper Marketing and Selling Points

Grants

These are non-repayable funds awarded for a specific purpose – for example grants may be awarded based on industry type, geography or social impact initiatives.

Unlike loans provided by financial institutions, which must be paid back with interest, grants are non-repayable funds given to various beneficiaries although there are strict conditions and eligibility requirements for how the money is to be used.

Grants:

Provide limited grants based on some thesis

Are purpose specific and have many eligibility requirements

By diversifying funding sources through these alternative options, companies gain the flexibility to support growth initiatives that are otherwise stifled by a reliance on traditional debt via banks or lending institutions.

While you work on improving your CIBIL score for a business loan, don’t miss out on opportunities like home loans in Coimbatore to secure a stable future.

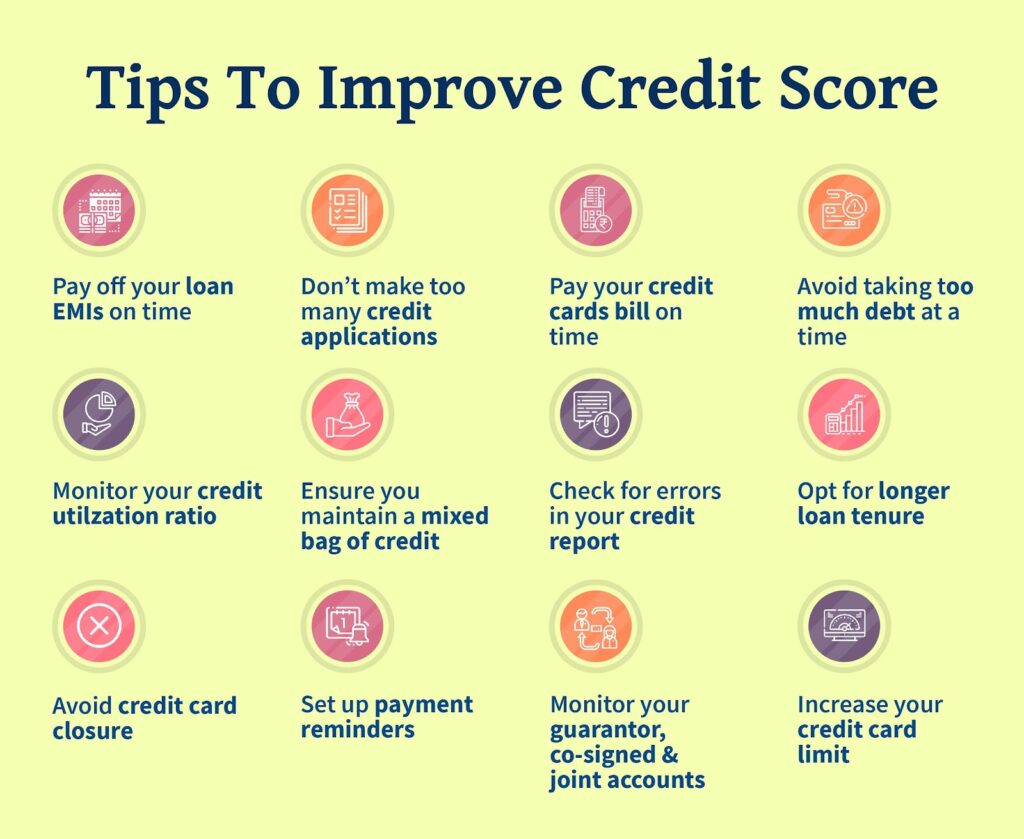

Tips to Enhance Your CIBIL Score for Better Loan Opportunities

Regularly Check

- And of course, with how you get to the point of applying for a business loan you should be monitoring your credit report anyways!

- Inaccuracies and distressing disclosures in this report can have a great impact on your CIBIL rating, may it can be loan rejection or unsatisfactory nethermost rates.

- By keeping track of your report and taking action to remedy any discrepancies, you are ensuring that the lenders get to see you in proper light.

- An accurate report means better loan availability

Responsible Financial Behavior

- Do engage in responsible financial behavior: As you can guess, responsible financial behavior is fundamental to improving and maintaining a good CIBIL score.

- One of the things that makes you a low risk applicant and positively affects your creditworthiness is having low credit card balances and being able to pay your bills on time.

- Applying for fresh credit every now and then: Applying for credit too many times within a short period could lead to multiple inquiries on your credit report and also bring down your CIBIL score.

- Be aware of these practices, and a part of your financial habit, you are working on increasing your creditworthiness in terms of the digits which represent that with the credit bureau.

Proactive Management

- Being aggressive in handling your finances will ensure that your CIBIL score does not take a hit. It requires maintaining good financial habits and also being alert and aware of when credit bureaus are alerted to changes or fluctuations in an individual’s credit report so that one can take immediate action to correct any inaccuracies.

- It takes an active approach that addresses problems before they have the opportunity to become bigger issues that could potentially impede their ability to secure business loans on advantageous terms.

Summary

Lenders set specific minimum credit score requirements for business loans, but in general, a higher score is more likely to lead to approval and better loan terms This is a particularly important concept for individual consumers to understand when thinking of how their credit score can impact their ability to get a loan and what they can do to improve that credit score to enhance their ability to get loans.

Frequently Asked Questions

What is the minimum CIBIL score required for a business loan?

Generally, lenders require a 700 and above CIBIL score to sanction a business loan. For some alternative lenders, scores as low as 600 may be acceptable for a loan, but rates could be much higher.

How does the credit score impact loan terms and interest rates?

A strong credit score leads to more favorable loan terms and lowered interest rates. A high credit score, which shows the lender that you are responsible with your credit and are more likely to receive more favorable terms on your loan.

Can I secure a business loan with a low credit score?

Sure, there are secured loan options out there, or alternative lenders who might be willing to take you on if your credit score is a bit lower. The catch is that these choices will likely at higher interest levels and for a bigger set of terms.

How can I improve my credit score for better business loan approval chances?

Lowering your credit utilization ratio, making on-time payments, and checking your credit report for inaccuracies can help raise your CIBIL score gradually. Any improvement to your overall credit profile by reducing existing debt is a step in the right direction.

Are there alternative financing options beyond traditional lenders for business loans?

Businesses do have access to other commercial financing alternatives such as peer-to-peer lending platforms, crowdfunding campaigns, invoice financing services and microloans from community development financial institutions (CDFIs). These are areas that meet the needs for all kinds of funding outside the scope of normal banking.