Securing a BusinessLoan Check out – What Credit Score is Needed Know the Credit Requirements of a Business Loan Your credit score to a large extent determines the possibility and conditions of getting a business loan.

Understanding the Importance of Credit Scores in Lending

Credit Score Ranges

Credit scores are among a lender’s main tools for making decisions on whether to approve or to deny business loan applications. Credit scores are used to assess whether a potential borrower is creditworthy and have a high chance of paying off their debt on time by the three main U.S. credit bureaus. The most widely used credit score model is FICO, which exists on a continuum from 300 to 850. In general, the higher the score, the less risk it represents and the better terms of borrowing it should result in.

An ideal credit score for a business loan is typically between 700 and 850. This is a range in which borrowers can generally expect to qualify for a loan with favorable interest rates and terms.

Impact of Credit History

Credit history is one the most common factors which affect a person’s credit score. It includes information about your prior and present debts, the way that you repay your debts, the outstanding balances on your credit cards and any negative marks, such as late payments or defaults. A credit history has an applicant’s financial activity, this is used as a minimal determination to if the applicant can manage their debts properly and understands financial responsibility.

Fast-track your business today to get funded. Discover business loan in Coimbatore. Unlock doors and get moving forward with certainty in your business.

Importance in Loan Approval

Qualifying borrowers with a reliable credit history are at the top of their list for lending institutions! By providing borrowers with access to more choices, a high credit score can lead borrowers to secure more favorable terms and conditions on the financing they receive.

On the flip side, people with good credit obtain business loans at banks with struggling credit policies greens become concerned that borrowers can not repay them as they have low credit scores.

Minimum Credit Score Requirements for Various Business Loans

Varying Loan Types

The credit score requirement can vary depending on the type of loan you choose For instance, the credit score required for a Small Business Administration (SBA) small business loan can vary from that of a traditional bank. All the loans have their own sets of qualities.

Before you apply for business loan, you need to familiar with the precise credit score requirements for each type of loan. This information assists small business owners in identifying areas where they can access loans as well as areas where they may need to improve their credit scores.

SBA Loan Credit Score Thresholds

The Small Business Administration (SBA) has their range of loan programs aimed for specific uses and scenarios. Some of these are its 7(a) program, geared towards general small business financing which is one of the most popular SBA loan programs, and microloans to help startups and businesses that are relatively new.

SBA loan programs have individual minimal credit score requirements that may affect the borrower’s eligibility drastically. A 7(a) program often has a minimum credit score in the mid-600s range, but microloans could be one way for entrepreneurs with lower or less established credit histories to gain access to essential funds.

Impact of Personal vs Business Credit Scores on Loan Eligibility

Distinction between Personal and Business Credit Scores

While personal credit scores hinge on an individual’s credit history, business credit scores are externalized in relation to the financial responsibility of the company at hand. When determining loan applications, lenders consider both.

Lenders usually take the owner’s personal credit score into account along with the overall creditworthiness of the business, when reviewing business loan applications. This can make up for a weaker business credit score.

How Personal Credit Affects Business Loan Eligibility

A good credit rating shows whether an individual is dependable in managing money, which in turn can leave a positive impact in a business loan application. For example, a small business owner might not have a credit history for their business, but their solid personal credit score could be used to secure the financing they need.

Conversely, a low personal credit score can make it difficult to get approved for favorable terms on a loan or get denied outright. As lenders see this as a potential warning that providing capital to this individual or their business represents some form of risk.

Building a Strong Business Credit Profile

To improve eligibility for future loans and better terms, businesses should focus on establishing and maintaining a robust business credit profile. This involves paying bills promptly and responsibly managing any lines of credit, among other factors.

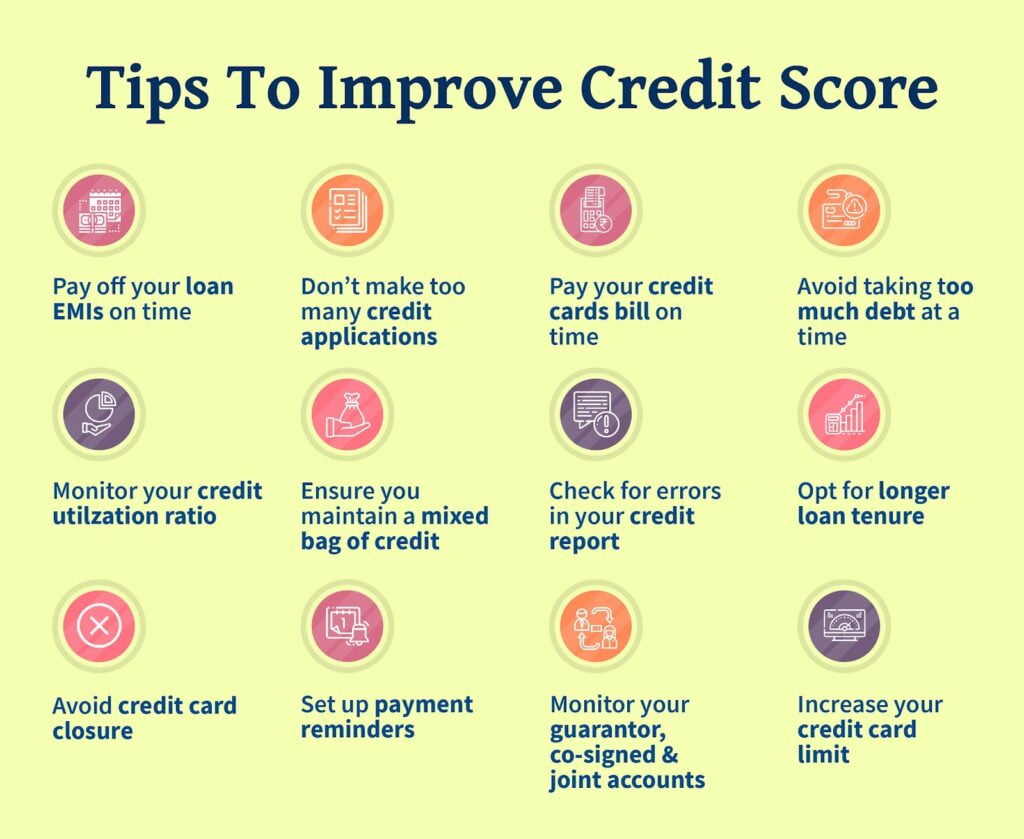

Strategies for Improving Your Credit Score Before Applying

Paying Bills on Time

Paying bills on time is vital to your credit score. Paying bills late can significantly damage your credit score because poor payment history is one of the primary determinants of a credit score. It shows the lender that you are responsible with your money and can be trusted with a loan.

Keeping and tracking a good history of on-time payments from previous debts such as your rent, utilities, and current loans, can also greatly help to increase your credit score in the long run.

This new balance will likely improve your credit score, and lowering your credit utilization ratio is a key part in doing that. This is the percentage of the credit available to you that you are using at any moment. Reducing it shows that you are using the credit made available to you in a responsible way and can be another tick in the right direction for your overall credit rating.

Checking for and Disputing Errors on Your Credit Report

It is important that you check your credit report for errors if you know you want to apply for a business loan. If the report has errors or inaccuracies, could unduly reduce your credit score and your chance of qualifying for a loan.

If you find any discrepancies during this review, such as accounts that are inaccurately reported as delinquent or wrong personal information, you should immediately dispute these errors with the pertinent reporting agencies.

Exploring Loan Options with a Suboptimal Credit Score

Alternative Financing

This alternative financing may be a good option. Such lenders tend to be more adaptable and are particularly open to working with those who have been shut down by conventional banks. Despite this, interest rates are high and this is a cost every entrepreneur has to bear, but this is the price you have to pay to get funds your business needs.

Other financing solutions include P2P platforms like Prosper or Lending Club. These platforms allow people to take out loans from investors instead of from typical financial institutions. This enables lighten personalized TOS meaning g more easily to be issued with poor credit.

Peer-to-Peer Lending

It is also an avenue for entrepreneurs with a poor credit to secure business loans. Via these platforms, borrowers can upload the details of their desired loan and level of risk, allowing investors to assess the risk and decide whether to fund the request.

They allow the parties to a transaction process (i.e. lenders and borrowers) to interact directly with each other and negotiate terms that are typically better than can be found through traditional sources of finance.

Microloans and Online Lenders

In particular, microloans from organizations like Kiva or Accion are designed to help out small business owners who have been denied funding elsewhere because of bad credit. While direct payday lenders with high approval rates do exist, this depends on the lender you want to take the loan out with, as most payday lenders have their own specific lending criteria, starting with faster credit checks.

Qualifying for a Business Loan with a Strong Credit History

Benefits of a Strong Credit History

A positive credit record goes a long way in ensuring that your business loan will be approved. Higher credit scores make borrowers look less risky and help borrowers seek the approval of lenders to loan applications. Businesses with a robust credit profile are eligible to secure more substantial loans at substantially lower interest rates. In other words, a good credit score increases the chances of being approved and comes with more competitive loan rates.

A borrower with a squeaky-clean credit score suggests it is more likely than not that they will repay borrowed funds, creating trust in the lender that the applicant will be able to repay them as well.

Negotiating Better Loan Terms with a High Credit Score

For example, when applying for funding through business loans, if you have a good credit score, you have greater bargaining power when it comes to negotiating with lenders. Strong credit candidates can use this fact to secure better terms, like;

- Reduced interest rates

- Longer repayment periods

- Higher borrowing limits.

They are more likely to provide a much better deal when you apply for a loan if you have an excellent credit history; this is because you are a low risk factor.

When businesses demonstrate responsible financial behavior, with a shining credit score, they can negotiate with suppliers more effectively for terms that make sense in the long run, and with minimal costs for the business.

Leveraging Assets to Secure Favorable Loan Terms

Besides a better chance of securing approval as well as better terms, strong businesses can also use performing assets as collateral to secure a secured business loan. Using an asset such as real estate or equipment to secure a loan not only reduces lender risk, but also allows for borrowers to obtain larger loan amounts than just off of their cash flow or revenue projections alone.

This model reinforces traditional cash flow based borrowing to avoid supply chain disruption while allowing credit-appropriate companies to use assets to secure financing to take advantage of favorable terms and incremental access to capital beyond cash flow only borrowing from lenders.

Leveraging Alternative Financing When Credit Scores Fall Short

Invoice Financing and Merchant Cash Advances

Invoice factoring and merchant cash advances Invoice factoring and merchant cash advances are financial tools targeted at business owners with tarnished credit. Invoice financing enables the business to sell its unpaid invoices to a third-party financial institution at a discount in exchange for fast-working capital.

This service isn’t dependent on credit score but rather on the value of the invoices. So, the process is similar to merchant cash advances, where businesses can receive an upfront amount of money by selling a percentage of the future sales at a discounted rate.

Equipment Financing with Lower Credit Requirements

One alternative option to secure funds for companies with low credit ratings, is the equipment financing. This arrangement makes the borrowed equipment security, and not the creditworthiness of the borrower. Because of the collateral, banks providing equipment financing are generally more lenient on bad credit.

Equipment financing allows business owners to purchase equipment or technology vital for operations despite their unfavorable credit situations.

Crowdfunding as an Alternative Funding Option

The method of crowdfunding has come to the fore as a unique practice of fund-fundraising in comparison with the conventional means of banks and other such traditional lending criteria. People can pitch there business ideas and projects to investors or donors online who in return for the exchange gives funds to that person in form of reward / equity.

This process avoids the need for robust personal credit history or large amounts of collateral that the majority of traditional lenders demand. It allows businesses with all sorts of scores to raise from customers who would like to see them succeed.

Tips for Elevating Your CIBIL Score for Future Loan Applications

Consistently Monitoring

Checking your credit report at least yearly is key to knowing how you are doing financially. First and foremost, it can alert you to any potential mistakes or problems that might be dragging down your credit score. This way, you will know what steps to take in order to fix any inaccuracies to make sure that your credit report is reporting the correct information.

You need to check your credit report with the three major credit bureaus: Experian, Equifax, and TransUnion. This systematic approach gives you an idea of how your credit standing would be perceived by lenders across every bureau.

Understanding your credit score is crucial for securing a business loan. If you’re also considering expanding your financial options, explore our home loans in Coimbatore for competitive rates and flexible terms

Utilizing Secured Credit Cards

If you want to rebuild or improve your credit, going with a secured credit card would be the way to go. Secured credit cards, however, involve a cash deposit, whereas unsecured cards do not, This will lower the threshold for those with lower scores to qualify, which is less risky for the lender.

When you use a secured card, and carry a balance properly (no need to justify yourself for getting a credit card) then you show that you are responsible with your finances. Over a period of time, this will help in increasing your CIBIL score and subsequently your credibility with future lenders for taking up any business loans or other forms of funding support.

Final Remarks

Bottom line, entrepreneurs need to stay busy when it comes to raising their credit scores for reasons giving them a shot at a kinder business loan. Following the approach listed in this article and answers from the professionals on how to build business credit, cannot only help to strengthen your creditworthiness, as but can also help in source funding requirement for the growth of your business.

Frequently Asked Questions

What is the significance of credit scores in business lending?

Lenders that follow traditional underwriting guidelines will have no interest in lending to borrowers with low credit scores. Credit scores are how lenders measure the amount of risk they are taking when lending money to a business and will likely set terms and interest rates accordingly based on these scores.

What is the minimum credit score required for different types of business loans?

Each lender and each type of loan may be different, but generally, conventional lenders may want to see a minimum credit score of around 680-700 for small business loans. But if you apply for alternative lenders or SBA-backed loans then they may approve with lower scores.

How does personal vs. business credit score impact loan eligibility?

It is in fact the case that lenders weigh personal and business credit scores differently when screening loan applications. Your personal credit score can compensate for a weak one on the business side, and different legal entities can prevent your personal assets from being attached to the performance of the company.

What are some strategies for improving one’s credit score before applying for a business loan?

Lowering your credit utilization ratio, paying down current debts on time, disputing errors on your report and reducing your debts can all help improve your credit score before you apply for a business loan.

When should businesses explore alternative financing options due to suboptimal credit scores?

When FICO scores are too low for approval for traditional financing options, businesses must seek alternatives with lenders who specialize in lending to businesses with “subprime” credit scores, or secured loans like merchant cash advances or equipment financing which is secured by the asset being purchased.